Will Chinese Banks Bail out More Indian Companies?

By Riaz Haq

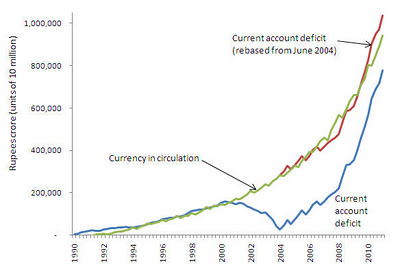

CA

India’s total external public debt has risen to $326 billion while foreign exchange reserves have dropped to $293 billion, according to the RBI data reported by the Indian Express newspaper.

The Reserve Bank of India is concerned over the increasing shift from equity to debt to fill India's widening current account gap. The latest available data indicates that foreign debt inflows in January so far have amounted to $3.21 billion versus $1.7 billion through equity inflows.

Recent $1.1 billion bail-out of Reliance Communications by state-owned Chinese banks is the clearest indication yet that the situation is also becoming dire in India's private sector with its mounting foreign debt.

This is not the first instance of Chinese banks coming to the aid of an Indian company. Last November, Sasan Power, the project company for the Sasan ultra mega power plant and a subsidiary of RComm affiliate Reliance Power, completed a $2.2 billion refinancing, including a $1.114 billion 13-year tranche. Bank of China, CDB and Chexim took $1.06 billion of that tranche, for which Chinese export credit agency Sinosure provided insurance.

Reliance Com is not alone in facing cash crunch in their ability to service debt. More than two dozen Indian companies included in the BSE-500 index face redemptions on foreign currency convertible bonds worth a combined Rs330 billion ($6.5 billion) by March 2013, according to brokerage Edelweiss. These include RComm’s US$925m outstanding CB, which the loan will repay.

Unless other Indian borrowers can somehow find lenders, they will be facing deteriorating debt market conditions that have led to shrinking liquidity in the loan markets and a rise in pricing.

“Top-tier Indian firms will have to pay between 250 basis points (2.5%) and 300 basis points (3.0%) over LIBOR (London Inter-bank Borrowing Rate) to borrow five-year money offshore. Even at that kind of pricing, there isn’t a lot of liquidity available,” said a Hong Kong-based lender quoted by International Financing Review. Over $20 billion worth of Indian debt is set to mature in 2012 and, of that, about $6 billion each of convertible bonds and rupee loans are up for redemption, with the balance in offshore loans.

India continues to run huge twin deficits of current account and budget. It depends heavily on foreign inflows. United Nations data shows that India received less than $20 billion in FDI in the first six months of 2011, compared to more than $60 billion in China while Brazil and Russia took in $23 billion and $33 billion respectively. Stocks in all four countries have underperformed relative to the broader emerging markets equity index, as well as the markets in the developed nations. Pakistan's KSE-100 has significantly outperformed all BRIC stock markets over the ten years since BRIC was coined.

Noting India's significant dependence on foreign capital inflows, Jim O'Neill recently raised concern about the potential for current account crisis. "India has the risk of ... if they're not careful, a balance of payments crisis. They shouldn't raise people's hopes of FDI and then in a week say, 'We're only joking'". "India's inability to raise its share of global FDI is very disappointing," he said.

In addition to Jim O'Neill, a range of investment bankers are turning bearish on India. UBS sent out an email headlined "India explodes" to its clients. Deutsche Bank published a report on November 24 entitled, "India's time of reckoning."

"Suddenly everything seems to be coming to a head in India," UBS wrote. "Growth is disappearing, the rupee is in disarray, and inflation is stuck at near-record levels. Investor sentiment has gone from cautious to outright scared."

India's current account deficit swelled to $14.1 billion in its fiscal first quarter, nearly triple the previous quarter's tally. The full-year gap is expected to be around $54 billion.

Its fiscal deficit hit $58.7 billion in the April-to-October period. The government in February projected a deficit equal to 4.6 percent of gross domestic product for the fiscal year ending in March 2012, although the finance minister said on Friday that it would be difficult to hit that target.

As explained in a series of earlier posts here on this blog, India has been relying heavily on portfolio inflows -- foreign purchases of shares and bonds -- as a means of covering its rising current account gap. Those flows are called "hot money" and considered highly unreliable.

Indian policy makers face a significant dilemma. If they do nothing to defend the Indian currency, the downward spiral could make domestic inflation a lot worse than it already is, and spark massive civil unrest. If they intervene in the currency market aggressively by buying up Indian rupee, the RBI's dollar reserves could decline rapidly and trigger the balance of payment crisis Goldman Sachs' O'Neill hinted at.

------------------------------------------------------------------------------